Debt Market Update

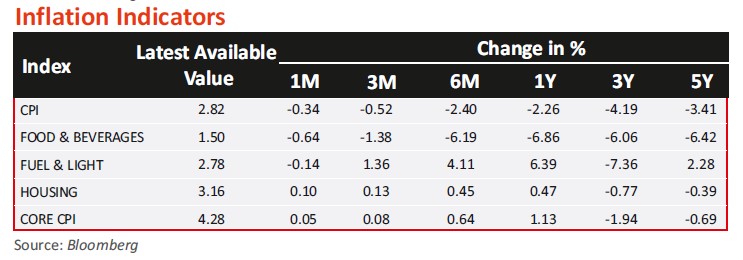

- June 2025 saw CPI inflation dropped to a six-year low of 2.10% (2.82% in previous month) driven by falling food prices, thanks to good harvests and improved supply chains. This stability has allowed the RBI more flexibility, following a 100 bps rate cut. While food inflation may stay low if favourable conditions persist, risks from weather and global shocks remain.

- India's WPI inflation rose to 2.61% in May 2025 (1.26% in April 2025), driven by steep food inflation—vegetables surged 32.4%, pulses 22%. Fuel inflation remained stable, while manufactured products saw marginal price increases. With wholesale price pressures building, policy uncertainty may persist despite retail inflation easing to a one-year low.

- Wholesale Price Index (WPI) inflation has been on a consistent downward trend since December 2024, touching (0.13%) in June 2025 (2.61% in May 2025) — a signal of softening input costs and improving economic momentum. Falling prices in key segments such as food, fuel, and manufactured products proved decisive.

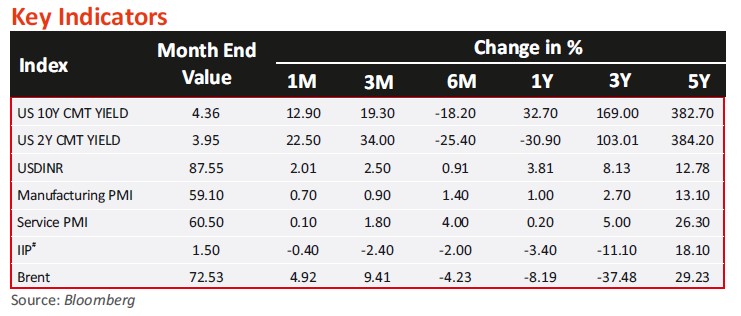

- Industrial growth (IIP) decelerated to 1.5% in June 2025, marking its weakest pace in ten months, primarily due to a severe contraction in the mining sector and continued weakness in electricity and primary goods. Mining output shrank by 8.7%, its lowest in nearly five years, while electricity contracted for the second straight month at 2.6%, a stark contrast to 8.3% growth seen in June 2024. The primary goods segment also performed poorly, with a 3% contraction—the worst in 56 months. However, manufacturing activity stood out, rising 3.9%, its best in five months, while intermediate and infrastructure goods posted notable gains of 5.5% and 7.2%, providing some cushioning to the broader industrial slowdown.

- India's gross GST collections climbed to Rs 1.96 lakh crore in July 2025, up from Rs 1.85 lakh crore in June 2025 and marking a 7.5% year-on-year increase. This rise, driven by stronger revenues from both domestic transactions and imports, points to continued economic resilience even as overall growth momentum moderates.

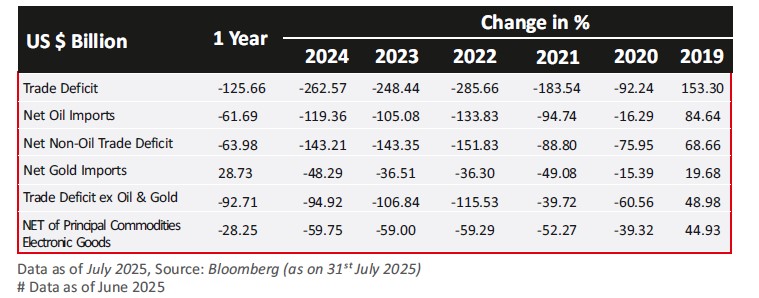

- India's trade deficit in goods narrowed to USD18.78bn in June 2025 (USD21.88bn in May 2025) —the lowest in four months—as imports fell more sharply than exports, basis provisional data. Exports stood at USD35.14bn, while imports declined to USD53.92bn, aided by falling gold and crude oil prices. Gold imports dropped to USD1.8bn from USD2.5bn, and crude oil to USD13.7bn from USD14.7bn. Total exports, including services, rose 6.5% to USD67.98bn, while overall imports edged up by 0.5% to USD71.50bn. This reduced the overall trade deficit to USD3.51 billion, down from USD7.30 billion in June 2024. Despite this monthly improvement, the April–June 2025 merchandise deficit widened year-on-year to USD67.26bn, though cumulative exports rose nearly 6% to USD210.31bn in the same period.

- Core sector growth rose marginally to 1.7% in June 2025 from 1.2% in May 2025, scaling a three-month high, yet remained well below robust levels, reflecting ongoing weakness in the economy. Five of the eight sectors contracted, with coal output plunging 6.8%—its worst in five years—while electricity and fertilisers also saw declines. The slowdown was attributed to excessive rainfall and high base effects. Steel and cement, however, benefited from strong government capital expenditure, recording solid growth of 9.3% and 9.2% respectively. Over the April–June 2025 quarter, core sector expansion slowed sharply to 1.3%, down from 6.2% last year.

Source: RBI, Bloomberg, CCIL, MOSPI

*BE - Budget Estimates

Past performance may or may not be sustained in future and is not a guarantee of any future returns, and should not be used as a basis of comparison with other investments. Index performance does not signify scheme performance Investors should consult their financial advisers if in doubt about whether the product is suitable for them.