Dear Partners

We stand at an interesting juncture in the markets today. The external environment is very volatile with high inflation, high energy prices and strong dollar. US Fed, at the recent Jackson Hole meeting, has indicated that it would continue to hike rates until inflation reduces to much lower levels and also that rates may remain higher for longer. At the same time, markets are fearing a possible recession in US sometime next year. With two other major economies i.e., the European Union and China already having weak economic growth, prospects of US recession is not good news.

We are also in the phase of transition to new, more environment friendly energy sources. Such changes take a very long time, may be a decade and in the interim, the transition phase creates its own issues. The demand for traditional energy sources viz. oil, gas and coal are still increasing. However, in last few years, there has been much lower investment in exploration and developments, leading to lower supply growth in oil and gas. This has led to increase in prices of oil and gas. To add to this, we have rising geo-political tensions on account of conflict between Ukraine and Russia and a possible rise in tensions between US and China over Taiwan. The resultant changes in supply arrangement and routes have led to even higher energy prices. So, Oil was already at around 80 dollars in December 21 and post the Ukraine conflict, it has moved up further.

We also have possible droughts in Europe and China, and some fear, which will lead to higher food inflation. High inflation in food and energy, two necessities of human race, can lead to lower disposable income in the hands of consumers and lower economic growth.

Against this backdrop of highly volatile macros, emerging markets in general have underperformed the developed markets. However, as we have been highlighting for last few months, India is much better placed to face this situation than most emerging markets and we may say even many developed markets.

- India's market share in global merchandise exports, which has been stagnant between CY10 to CY20, increased in CY21. Global trends such as China plus one strategies and Governments policies such as PLI are likely to lead to better export performance to fund our energy import bill. IT exports and remittance remain strong.

- Thus, even with Crude oil at around USD 100-120/barrel, Current account deficit for FY23 is likely to be around 3.5% of GDP, much lower than the 4.5% levels seen in FY12-13.

- Despite high energy prices and some slowdown in developed market economies and Chinese economy, India's economic growth remains strong as reflected in various indicators such as PMI numbers, electricity consumption, GST collections, property registrations etc.

- Our fiscal situation remains in control, with tax collections remaining strong.

- Fiscal deficit, though higher than pre-Covid levels is oriented towards higher capital expenditure.

- Forex reserves are high at around USD 560 bn. External debt levels remain low. Forex reserves are strong and adequate to meet the projected CAD and external debt payments.

- Inflation differentials between India and developed world are much lower than the levels seen in FY12-13. Thus, while interest rates are likely to rise, the degree of liquidity tightening is likely to be much lower than seen in the previous periods of rate upcycle.

- India's corporate sector is in good shape. Aggregate profits of NSE 500 companies are set to double from Rs 5.20 lac crores in FY19 to over Rs 10.6 lac crores in the current year i.e., FY23. Leverage levels of corporate sector are low.

- India's banking sector is in good health, banks are well capitalised, historical NPAs are provided for. Despite Covid led disruptions, asset quality has held up well.

- India's economy has gone through a host of disruptive reforms viz. demonetisation, GST, RERA, the insolvency and bankruptcy law code and has now stabilised.

- With both corporate and banking sector in good shape, we feel India is at the cusp of start of a domestic economic recovery cycle, which can lead to multi-year growth.

Last two months, we have had a rally in equities across the world. The rally was based on the premise that a cooloff in inflation as reflected in falling prices of most metals, and expectations of an early end to the rate hike cycle by US Fed. The recent comments by US Fed at Jackson Hole have to some extent, dashed these hopes.

Valuations of equity markets after the recent rally are at above historical averages. Also, high inflation and energy prices, have led to some downgrade in Nifty earnings. We feel that the recent volatility in equity markets would continue for some more time, may be for another four to five months.

As the global macro situations resolves, Indian economy is in a strong position to bounce back. We feel the domestic cyclicals, be it consumption oriented or investment oriented, would lead the economic recovery. The key advantage India has over many emerging markets is that we have a strong domestic demand base, and our economy is less dependent on exports and global commodity cycles.

Thus, domestic cyclicals such as auto and auto ancillaries, consumer durables, real estate and building materials, capital goods and engineering, infrastructure related sectors should do well. Within defensives, pharma and healthcare sector should do better as it comes out of a low growth phase.

How are we positioned in our funds?

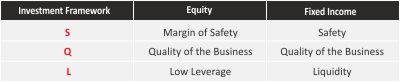

With macro situation being very dynamic and volatilities across asset classes increasing, we continue with our strategy of running well diversified portfolios. We are more focused on stock selections within the sector rather than trying to take large overweight / underweight positions among sectors. The focus continues stock selection on a bottom-up basis anchored on our “SQL Investment Framework”

What should be your approach while investing into our Mutual Fund Schemes?

We expect the volatility to continue over the next few months as the market-outlook is likely to remain challenging. With markets having seen a good bounce back in last three months, valuations have again moved above long-term averages. Some sections of the market feel that a fall in energy prices should be beneficial to India. However, a look into the past suggests that whenever crude has corrected due to demand destruction in economic recessions, India's earnings growth and market performance have not remained immune. If crude prices correct due to increase in supplies, India will definitely benefit.

Investors wanting to invest in lumpsum should invest in ITI Balanced Advantage Fund. More conservative investors can invest in the ITI Conservative Hybrid Fund, which has the potential to give better returns than traditional savings products and with much lower volatility than that of equity or aggressive hybrid funds.

Investment in equity funds, particularly mid and small cap categories, should be done systematically over the next three to four months in the form of daily / weekly STPs or SIPs.

Our Investment Philosophy – SQL

Based on our combined investment learnings of more than 50 years, we have institutionalized very strong and unique investment Framework -SQL, which is core to our fund management framework and approach to our portfolios. We strongly believe that good quality (Q), low leverage companies (L) bought with a reasonable good margin of safety (S) makes the investment very attractive and rewarding for our investors.

Our Risk Management Framework

Our Risk Management Framework & our unique Investment Framework are well thought-out and institutionalised to generate superior investment performance and creating a smooth investment experience for all our investors. They are framed based on our own investment experience and also imbibed learnings from some of the great investment houses and investment managers globally, which will stand the test of time and keep our investors interest at high standards. We have put risk limits based on fund mandates, market cap segments, sectors and stocks.