Dear Investors & Partners,

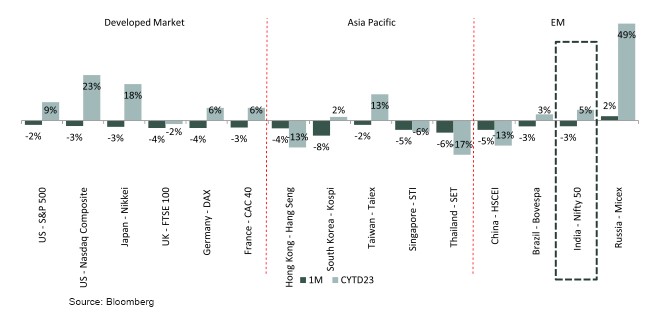

Indian equity markets flagship Nifty-50 was down 3% MoM in Oct-23. Small cap and mid cap indices were down by 2% & 4% respectively. Except Realty (+5%) all other sectors witnessed negative returns MoM in Oct-23.

Globally too, stock indices were weak in Oct-23 even after weakness seen in Sep-23. S&P 500 and Nasdaq decreased by 2% and 3% respectively, while most of the indices declined by 2-8%.

Sustained earnings growth crucial for valuations to sustain:

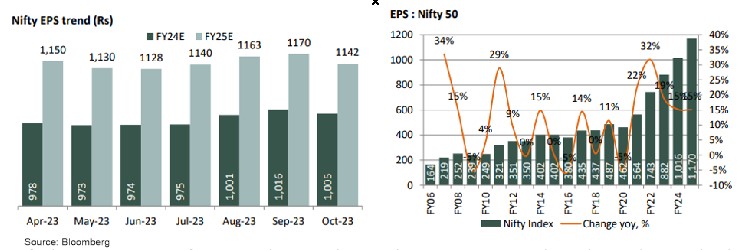

Midway through earnings season, the Nifty-50 EPS for FY24E/FY25E is marginally lower by 1-3% for FY24/25E, but earnings growth expectations in FY24-25E remains strong and expectation is Nifty-50 EPS to increase by ~15% YoY each for FY24E and FY25E.

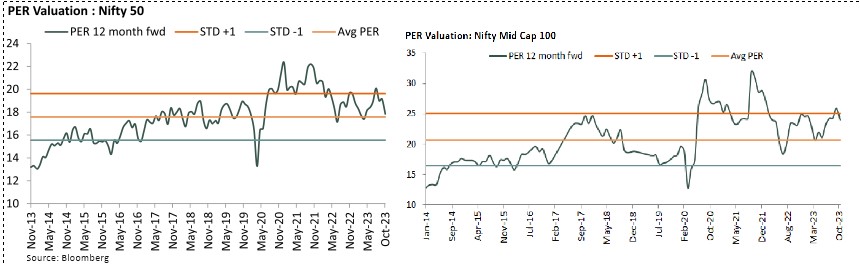

Regardless of valuation concerns, Nifty-50 is trading on its historical averages. However, the Mid cap index is trading higher than its historical averages and the Mid cap valuation premium has moved up in FY24E.

While most of India's domestic growth paramters like GST (Goods & Services Tax) collection, PMI, (Purchasing Manager’s Index) e-way bill data, electricity demand, rail traffic, etc continue to be healthy, there can be some near-term hiccups. These include possibility of volatile food inflation numbers, high global uncertainty, sustained higher interest rates globally, and negative FPI flows for the second month in a row. Further state elections in 5 states, to be follwed by central elections next year can lead to delayed policy making or diversion of focus away from constructive policy making if the worse case scenario is considered.

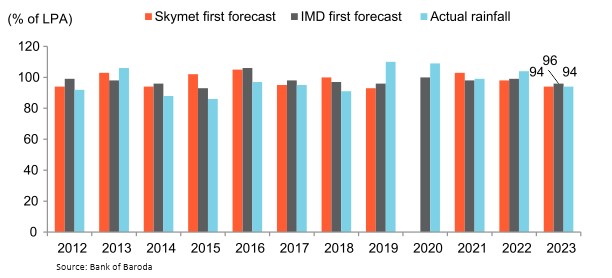

El Nino bullet dodged, but actual rainfall below normal:

India witnessed below normal rainfall in 2023 after witnessing normal and above normal rains rainfall in the preceding 4-years, with a deficiency of 6% below its Long Period Average (LPA). Rainfall was deficient across two regions - South Peninsula (92% of LPA) and North East (82% below LPA). Rainfall in North West and Central region stood 101% and 100% respectively of LPA.

El Nino, which is the warming of waters in the Pacific Ocean near South America, is associated with weaker monsoon winds and drier conditions in India. The El Nino bullet was dodged as far as India was concerned in 2023 as despite fears of El Nino impacting rainfall and an unusually dry August, rainfall turned out to be just marginally lower than last year.

As per the Indian Meteorological Department (IMD), currently, moderate El Nino conditions are prevailing over the Equatorial Pacific Ocean and positive Indian Ocean Dipole (IOD) conditions are prevailing over the Indian Ocean. These are likely to continue during the upcoming season, but positive IOD conditions are likely to weaken during the upcoming months. Though very early, it is possible that El Nino might weaken April onwards and may not influence Indian 2024 monsoon season in a big way. If this early forecast turns out to be accurate it will be a major positive for Indian agriculture as well as the economy.

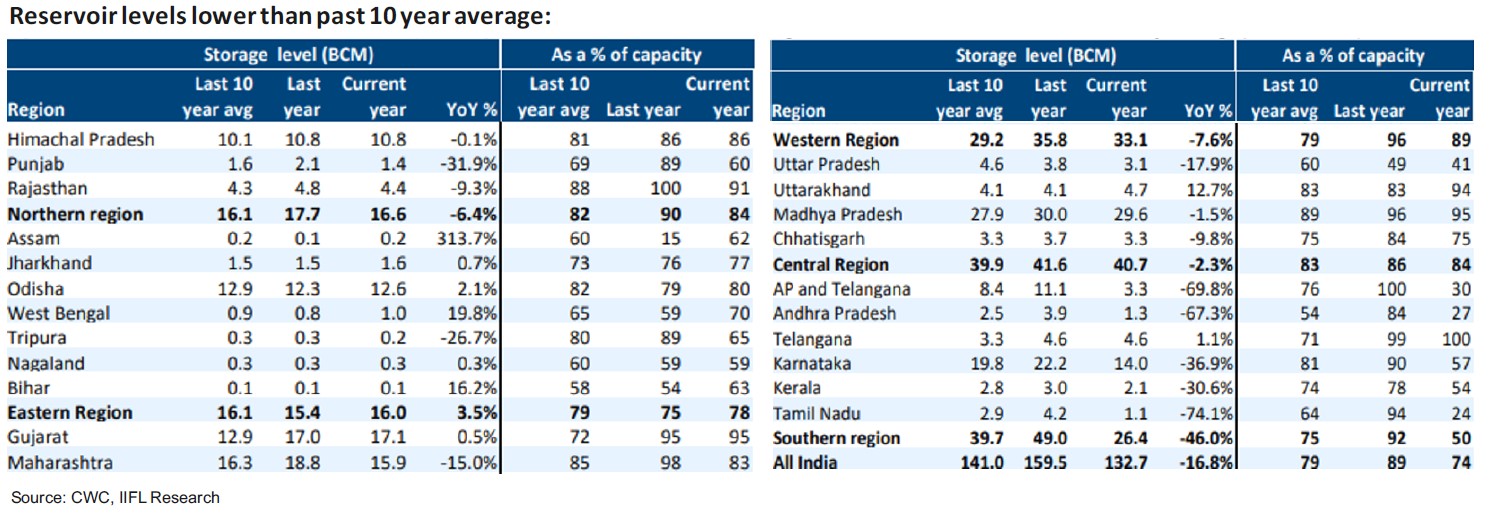

Reservoir levels in South and East India are at a deficit to average levels, which could impact sowing patterns during Rabi. Reservoir levels in Maharashtra too, are down 15% YoY. Crops whose output can be impacted are sugarcane, rice and some coarse cereals. As of 5th October, reservoir levels were below the past 10 year average.

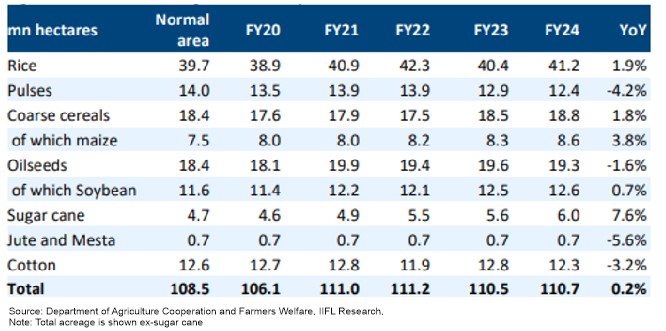

Kharif acreage marginally higher, but output may be lower:

While the overall acreage sown was marginally up YoY, acreages for pulses were lower by ~4%. This was offset by the higher acreage in rice and maize. As a result of the weaker-than-expected monsoon, production of rice and major kharif crops could also see a dip, according to the first advanced estimate released few weeks back.

Higher for longer concerns

The top three economies in the world had recently overshot GDP expectations (Q3 - US: 4.9%, China: 4.9% YoY; Q2 - Japan: 6% annualised), although the European Union GDP growth was muted at 0.1%, while India's GDP has upside risks given the robust high frequency indicators in terms of PMI, tax buoyancy, corporate profits, IIP, credit growth, electricity demand etc. The aforementioned trends indicate global GDP growth outlook has upside risks. The expectation of a rate cut in the near term is being replaced by 'higher for longer' paradigm given the robust growth and elevated but declining inflation. Further rise in interest rates hereon remains a key risk to economic growth and valuations of equities relative to bonds.

Center's fiscal remains well-balanced

The Center's fiscal deficit in 1HFY24 (Half Financial Year 23-24) remained in check at 39% of FY2024BE, aided by an improvement in direct tax collections. The pace of expenditure remained steady and buoyed by capex on roads and railways. We expect the Center to adhere to its FY2024BE GFD/GDP target of 5.9%, given robust tax collections, the RBI's surplus transfer and manageable expenditure, so far.

The Center's total receipts (including divestments) were at 52% of FY2024BE in 1HFY24 (18% higher than 1HFY23). Gross tax revenue improved to 48% of FY2024BE (16% higher), driven by direct tax growth at 25% in 1HFY24 (with corporate and income tax growth rates at 20% and 30%, respectively). Net tax revenue in 1HFY24 was at 50% of FY2024BE (15% higher).

Expenditure in 1HFY24 was at 47% of FY2024BE (16% higher than 1HFY23). Capex was at 49% of FY2024BE (43% higher), with (1) roads at 60% of FY2024BE (28% higher), (2) railways at 59% of FY2024BE (61% higher) and (3) loans to states at 46% of FY2024BE. Revenue expenditure was at 47% of FY2024BE (10% higher than 1HFY23). Overall, fiscal deficit in 1HFY24 was comfortable at 39% of FY2024BE (1HFY23: 37% of FY2023BE).

GST collections for September (collected in October) were 13.4% yoy higher at Rs1.72 trillion (August: Rs 1.63 tn), with CGST at Rs301 bn (Rs298 bn), SGST at Rs382 bn (Rs377 bn), IGST at Rs913 billion (Rs836 bn) and compensation cess at Rs125 bn (Rs116 bn). CGST collections are at a monthly run-rate of Rs664 bn in 7MFY24; in line with the required run-rate of Rs694 bn to meet the FY2024BE target.

Festival demand will be crucial

The ongoing festival season which also coincides with the harvest time in rural areas will be crucial. The performance of industry in the first 5 months of the year has been steady with growth in IIP (Index of Industrial Productions) at nearly 6.1%. Consumer goods however have grown at just 4%, which is the same as last year. The actual scenario once the period ends should give a much clearer picture on urban spending patterns and whether the rural economy has bottomed out.

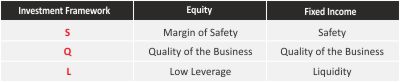

Our Investment Framework – SQL

Based on our combined investment learnings of more than 50 years, we have institutionalized very strong investment Framework -SQL, which is core to our fund management framework and approach to our portfolios. We strongly believe that good quality (Q), low leverage companies (L) bought with a reasonable good margin of safety (S) makes the investment very attractive and rewarding for our investors.

Our Risk Management Framework

Our Risk Management Framework & our Investment Framework are well thought-out and institutionalised to generate superior investment performance and creating a smooth investment experience for all our investors. They are framed based on our own investment experience and also imbibed learnings from some of the great investment houses and investment managers globally, which will stand the test of time and keep our investors interest at high standards. We have put risk limits based on fund mandates, market cap segments, sectors and stocks.

How are we positioned in our funds?

With macro situation being very dynamic and volatility increasing across asset classes, we continue with our strategy of running well-diversified portfolios. We are more focused on stock selection process within the sector rather than trying to take large overweight / underweight position among sectors. The focus continues to be on stock selection on a bottom-up basis anchored on our “SQL Investment Framework”.

Top 2 overweight sectors in our equity schemes are as under:

- Multicap fund: Capital goods, Consumer Services

- ELSS Tax saver: Realty, Consumer Services

- Small cap fund: Capital goods, Autos

- Large cap fund: Autos, Construction material

- Mid cap fund: Capital goods, Autos

- Value fund: Capital goods, Consumer durables

- Flexicap fund: Capital goods, Autos

- Focused Equity: Capital goods, Autos

What should be your approach while investing into our Mutual Fund Schemes?

We expect the volatility to continue over the next few months as the market-outlook is likely to remain challenging. Valuations remain marginally above long-term averages. On the back of lower commodity prices and with operating leverage, earnings would rise for corporates and rupee denominated trade could lead to a strong performance by the Indian economy in Fy24.

Investors wanting to invest in lumpsum can invest in ITI Balanced Advantage Fund, Value Fund and ITI ELSS Tax Saver Fund (formerly known as ITI Long Term Equity Fund). Investment in equity funds, particularly mid and small cap categories, should be done systematically over the next three to four months in the form of daily / weekly STPs or SIPs. While the current rally shows little signs of slowing down, retail investors must continue investing in well-managed funds via SIPs.

What should be your approach while investing into our Mutual Fund Schemes?

We expect the volatility to continue over the next few months as the market-outlook is likely to remain challenging. Valuations remain marginally above long-term averages. On the back of lower commodity prices and with operating leverage, earnings would rise for corporates and rupee denominated trade could lead to a strong performance by the Indian economy in Fy24.

Investors wanting to invest in lumpsum can invest in ITI Balanced Advantage Fund, Value Fund and ITI ELSS Tax Saver Fund (formerly known as ITI Long Term Equity Fund). Investment in equity funds, particularly mid and small cap categories, should be done systematically over the next three to four months in the form of daily / weekly STPs or SIPs. While the current rally shows little signs of slowing down, retail investors must continue investing in well-managed funds via SIPs.