Dear Investors & Partners,

Equity market performance in May'24

Over the last 12 months, global market cap increased 14% (USD14.4TN), whereas India's market cap surged 40%

DII (Domestic Institutional Investor) inflows remain strong; FIIs (Foreign Institutional Investors) record the second consecutive month of outflows: DIIs recorded the ten consecutive month of inflows in May'24 at USD6.7BN. FIIs recorded outflows of USD3b in May'24. FII outflows into Indian equities stand at USD2.8b in CY24YTD vs. inflows of USD21.4b in CY23. DII inflows into equities in CY24YTD continue to be strong at USD25b vs. USD22.3b in CY23.

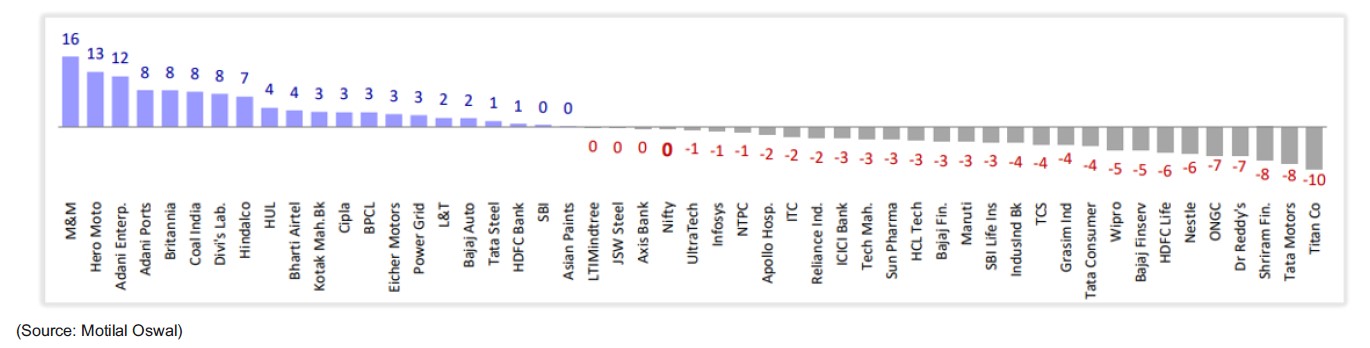

Breadth adverse in May'24: Among sectors, Capital Goods (+11%), Utilities (+7%), Metals (+6%), Real Estate (+5%), and Automobiles (+4%) were the top gainers, whereas PSU Banks (-3%), Technology (-2%), Private Banks (-1%), Media (-1%), and Healthcare (-1%) were the top laggards MoM. M&M (+16%), Hero Motocorp (+13%), Adani Enterp. (+12%), Adani Ports (+8%), and Britannia (+8%) were the top performers, while Titan (-10%), Tata Motors (-8%), Shriram Finance (-8%), Dr Reddy's (-7%), and ONGC (-7%) were the key laggards. Major economies end lower in May'24: Among the key global markets, the US (+5%), Taiwan (+4%), the UK (+2%), ended higher in local currency terms. However, Russia MICEX (-9%), Indonesia (-4%), Brazil (-3%), Korea (-2%), China (-1%) ended lower MoM in May'24. Over the last 12 months, the MSCI India Index (+31%) has significantly outperformed the MSCI EM Index (+9%). Over the last 10 years, the MSCI India Index has outperformed the MSCI EM index by a robust 197

Valuations:

At the present level of valuations, the valuations of NIFTY is in-line with 1-year forward earnings of last 10 years while on a P/BV ratio, it is higher than the 10-year average multiples

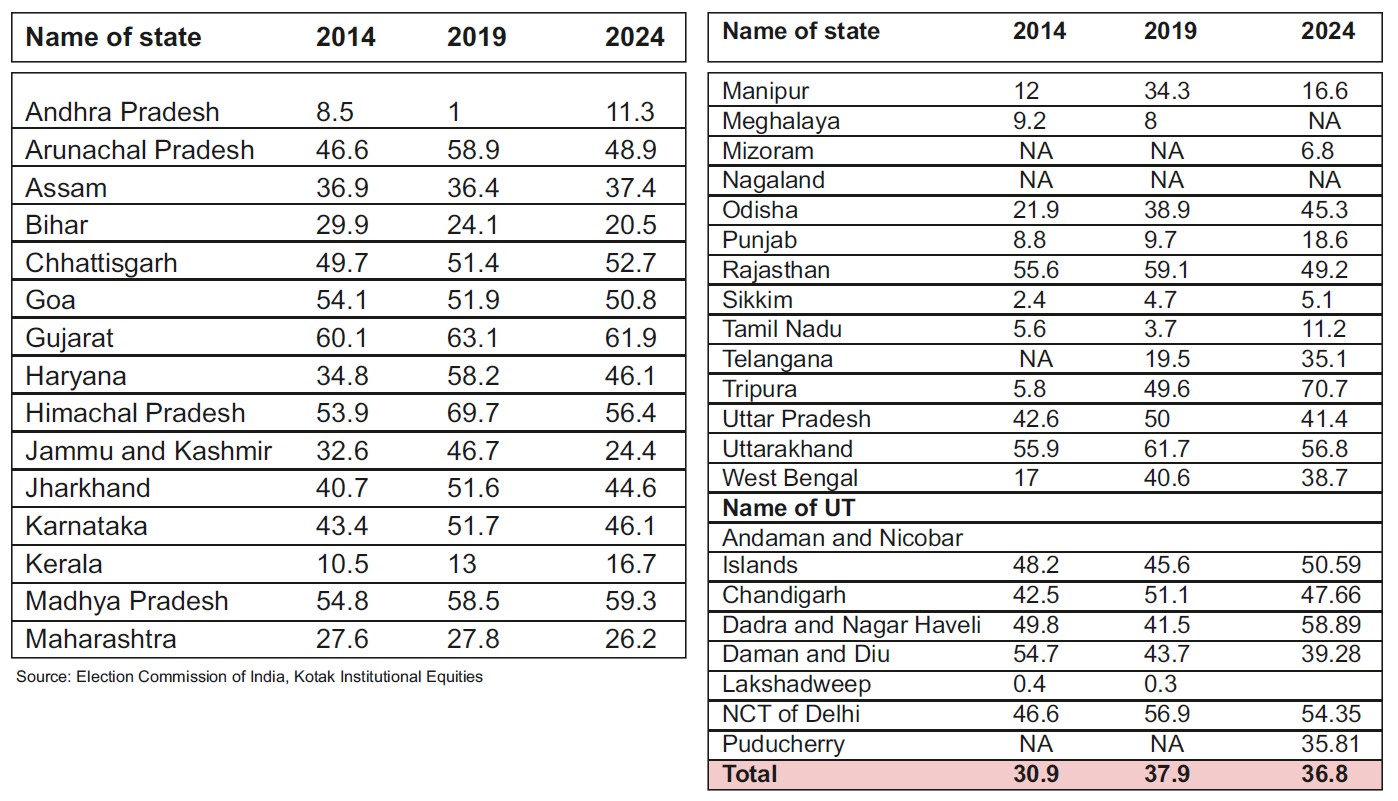

Outcome of General Elections: The key event to watch out for were the outcome of the general elections. The incumbent current Prime Minister is set to assume the office for a third consecutive term. This assumes significant importance considering the fact that after a gap of six decades (Prime Minister achieved this feat in the year 1962), current Prime Minister is the only Prime Minister to assume the office for third consecutive term.

While the current Goverment would have secured 63 seats lesser compared to 2019, the party has lost just ~110 bps of vote share compared to FY19 but ex-Uttar Pradesh, current ruling party hasgained vote share on Pan-India basis.

There was significant volatility witnessed in the market, with NIFTY registering the biggest fall in last 4 years, with the news that current ruling party secured 240 seats in the current Loksabha Elections raising question mark on the stability of the Government over the next 5-year term. However, it should be noted that opposition completed full 5-year term, both in 2004 and 2009 elections securing 145 seats and 206 seats respectively.

While all eyes would be on the Government's 100-day agenda, we expect that the focus on capital goods, infra sector would continue despite the media reports about focus on populist measures in upcoming budget. The recent dividend of more than Rs.2 lakh crore by the RBI should act as a buffer and help the Government strike an effective and efficient balance between growth and populism.

Structural positive macro view remains intact:

1. Positive commentary from the RBI: The RBI in its latest policy update has upgraded the real GDP growth forecast from earlier 7% forecast to the latest 7.2% for FY25.

2. Strong earnings trajectory: The recently concluded result season registered not only strong growth being reported by manufacturing companies (a trend being prevalent for quite sometime) but also positive commentary by major companies catering to the rural markets – FMCG, 2-wheeler, tractors.

3. Forecast of above normal monsoon: Above-normal rain will help the country improve its agricultural output and replenish water reservoirs at a time when several regions have faced severe heatwaves with the temperature going as high as over 49°C. The forecast comes as a relief after uneven precipitation and prolonged dry spell last year due to El Nino weighing on the farm sector.

The southwest monsoon rainfall over the country during June-September is likely to be 106% of the long period average.

4. Interest rate reduction should commence in 2HCY24: The European Central Bank (ECB) cut interest rates by 25 basis points, lowering its deposit rate to 3.75%. This had been at a record high and saw the ECB joining the likes of Canada, Sweden and Switzerland in lowering rates.

US Federal Reserve officials plan to reduce key interest rates three times in 2024 despite higher inflation, though the quantum and the beginning of the same is not year certain. However, its increasingly likely that the interest rate cycle has peaked.

Our View

India is currently enjoying the confluence of the macro and micro tailwinds with ~7% GDP growth, moderating inflation prints, range-bound crude prices, easing 10-year G-sec yield, stable currency, and resilient corporate earnings.

Earnings growth trajectory, capex, policy initiatives like PLI, etc. and the timing and quantum of interest rate easing globally, will be the key monitorable for sustained valuations and market growth. This is even as India has outperformed the MSCI index.

The incumbent Government is expected to continue for the third term, the focus would shift on the upcoming Union Budget. While there are nascent indications of rural demand bottoming out, it is too early to call out a recovery for certain.

We continue to believe that the investment environment going forward would be a “stock picker's market” and would separate the men from the boys. There could be instances where companies operating in the same sector may end up reporting diverse set of financial results. Our approach in such an environment would be the same as we have been following over the last few quarters. It would revolve around the thesis to identify companies basis the “bottom up” approach.

Our Risk Management Framework & our Investment Framework are well thought-out and institutionalised to generate superior investment performance and creating a smooth investment experience for all our investors. They are framed based on our own investment experience and also imbibed learnings from some of the great investment houses and investment managers globally, which will stand the test of time and keep our investors interest at high standards. We have put risk limits based on fund mandates, market cap segments, sectors and stocks.

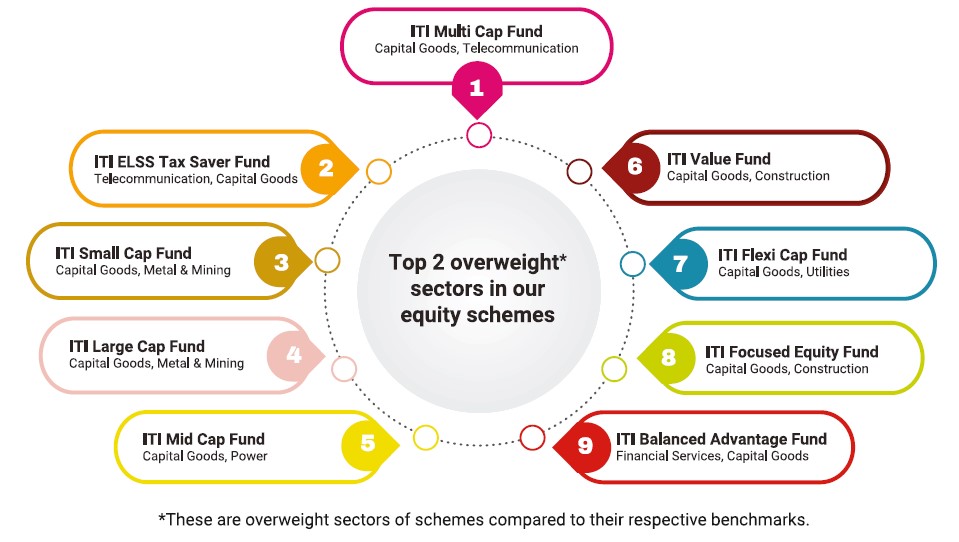

How are we positioned in our funds?

With macro situation being very dynamic and volatility increasing across asset classes, we continue with our strategy of running well-diversified portfolios. We are more focused on stock selection process within the sector rather than trying to take large overweight / underweight position among sectors. We would also refrain from taking aggressive cash calls.

What should be your approach while investing into our Mutual Fund Schemes?

We expect the volatility witnessed in the month of YTD CY24 to continue over the next few months as the market-outlook is likely to remain challenging. Valuations remain marginally above long-term averages. On the back of stable commodity prices especially crude oil and with operating leverage, earnings would rise for corporates and rupee denominated trade could lead to a strong performance by the Indian economy in CY24.

Investors wanting to invest in lumpsum should invest in ITI Balanced Advantage Fund, Value Fund and ITI ELSS Tax Saver Fund (formerly known as ITI Long Term Equity Fund). Investment in equity funds, particularly mid and small cap categories, should be done systematically over the next three to four months in the form of daily / weekly STPs or SIPs. While the current rally shows little signs of slowing down, retail investors must continue investing in well-managed funds via SIPs.